Illinois is one of only three states that does not tax retirement income. That cost the state $2.2 billion in FY 2013, and along with other tax breaks the total revenue the state is foregoing is close to $9 billion. Is it time to reassess and end at least some of these tax breaks? Laurence Msall, president of the Civic Federation, is just back from Springfield and joins us to share his thoughts.

Budget Negotiations

In March, the Illinois Legislature approved a stopgap budget to plug a $1.6 billion hole in the current fiscal year. Now, legislators and Gov. Bruce Rauner are focused on the upcoming Fiscal Year 2016 budget which includes a $6.6 billion budget gap and begins on July 1.

Pensions

Pensions

Rauner’s pension reform package includes maintaining all currently earned benefits to date, moving all future work into the Tier 2 pension plan, and providing an optional buyout to reform cost-of-living adjustments in return for a 401(k)-style defined contribution plan. Under the governor’s plan, Tier 1 members will have their Tier 1 service frozen on July 1, and going forward all service will be in Tier 2.

Tier 2 benefits include retirement age of 67 (with 10 years of service), annuity based on highest eight out of last 10 years of service, and cost-of-living adjustments equal to the lesser of 3 percent or one-half of the annual increase in CPI, not compounded. If all four retirement systems—State Employees’ Retirement System, State Universities’ Retirement System, Teachers’ Retirement System, General Assembly Retirement System—are reformed per the governor’s plan there will be a reduction of $2.2 billion in contribution. Rauner’s reforms are also contingent on an amendment to the state constitution.

Rauner’s projected savings from pension reform have been met with skepticism by lawmakers. Tuesday, Senate President John Cullerton told Chicago Tonight that the governor can’t count on those savings because of the difficulty of passing pension legislation and lawsuits that could be the result of any passed legislation.

A Chicago Tribune article outlines how Rauner’s proposed pension fix could backfire, highlighting a 2010 law that cut the cost of pensions offered to newly hired state workers and teachers. The Tribune reported “the reductions for new hires were so steep that by 2027 retirement benefits for some workers will begin to fall below minimum federal standards, exposing taxpayers and employees alike to expensive repercussions.” Workers hired in the last five years may end up contributing more into the pension system during the course of their careers than the projected benefits they could receive one day, according to the Tribune.

Tax Expenditures

Tax Expenditures

Every year, the State of Illinois Comptroller releases a tax expenditure report. According to the comptroller’s office, “a tax expenditure is any exemption, exclusion, deduction, allowance, credit, preferential tax rate, abatement, or other device that reduces the amount of tax revenue that would otherwise accrue to the State.”

The most recent report issued last April says state agencies reported 273 tax expenditures, totaling approximately $8.9 billion in forgone revenues in Fiscal Year 2013. According to the report, tax expenditures have been used since the early 1930s and really expanded during the 1980s. Of the 273 tax expenditures for FY2013, 225 were associated with taxes and 48 with licenses or fees.

Tax expenditures for FY2013 were up 7.1 percent from FY2012, with much of the increase due to a newly reported corporate income tax Foreign Dividend Subtraction (which is a subtraction of dividends received by a foreign corporation). Tax expenditures for individuals totaled $5.9 billion, while businesses received $2 billion and charities received $348 million.

View a chart of the Top 15 largest tax expenditures which account for $7.833 billion of the total $8.95 billion in tax expenditures for FY2013.

| Expenditure | Amount | Applied Against |

|---|---|---|

| Retirement and Social Security Deductions | $2.233 billion | Individual Income Tax |

| Food, Drugs, Medical Appliances | $1.644 billion | Sales Tax |

| Standard Deduction | $1.110 billion | Individual Income Tax |

| Property Tax Credit | $548 million | Individual Income Tax |

| Foreign Dividend Subtraction | $360 million | Corporate Income Tax |

| Sales to Exempt Organizations | $333 million | Sales Tax |

| Exemption for Trade-Ins | $282 million | Sales Tax |

| Farm Chemical Exemption | $267 million | Sales Tax |

| Manufacturing Machinery Exemption | $204 million | Sales Tax |

| Hospital Provider Exemption | $173 million | Hospital Provider Assessment |

| Earned Income Tax Credit | $162 million | Individual Income Tax |

| Gasohol Discount | $146 million | Sales Tax |

| Biodiesel Discount and Exemption | $133 million | Sales Tax |

| Retailer's Discount | $125 million | Sales Tax |

| Non Motor Vehicle Use | $114 million | Motor Fuel Tax |

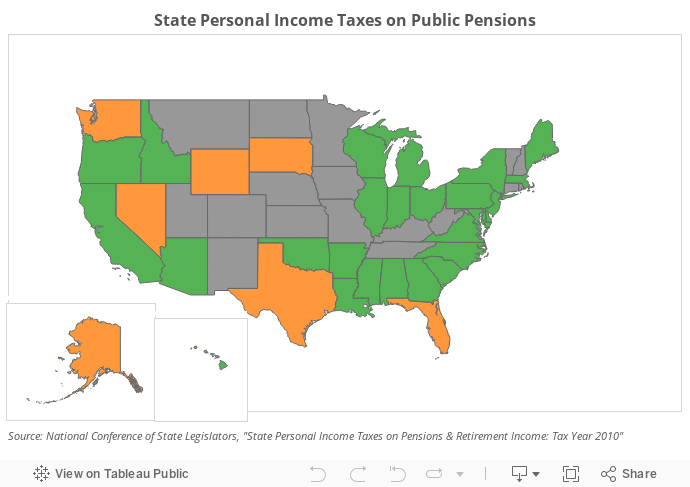

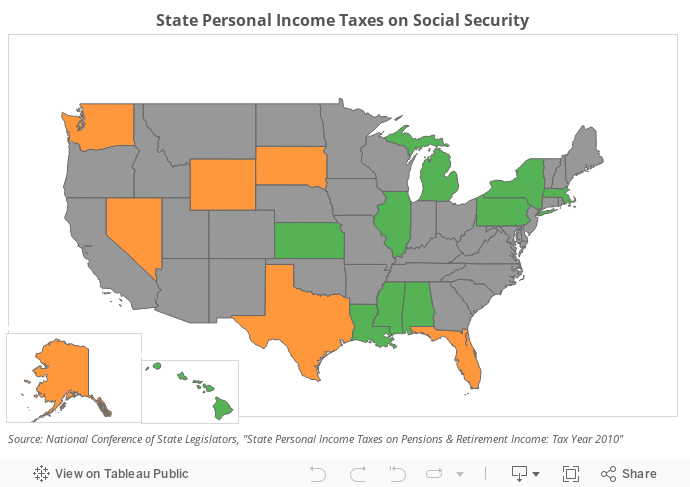

According to the report, the tax expenditure for retirement income, such as Social Security, pensions, and IRAs, was the largest expenditure for FY2013, totaling $2.233 billion. Illinois is only one of three states that do not tax retirement income (public pensions, Social Security, and private pensions); Mississippi and Pennsylvania are the other two. These three states are the only states to provide full exemptions for private pensions.

View the maps below to see how states tax public pensions and Social Security. States colored orange do not levy a personal income tax. States colored green provide full exemptions from taxation, while states colored gray tax retirement income at some level.

{kind=link}